Null hypothesis: data follows a time series model using auto.arima from the forecast package

null_ts(var, modelfn)Arguments

- var

variable to model as a time series

- modelfn

method for simulating from ts model.

See also

null_model

Examples

require(forecast)

#> Loading required package: forecast

#> Registered S3 method overwritten by 'quantmod':

#> method from

#> as.zoo.data.frame zoo

#> Registered S3 methods overwritten by 'forecast':

#> method from

#> autoplot.Arima ggfortify

#> autoplot.acf ggfortify

#> autoplot.ar ggfortify

#> autoplot.bats ggfortify

#> autoplot.decomposed.ts ggfortify

#> autoplot.ets ggfortify

#> autoplot.forecast ggfortify

#> autoplot.stl ggfortify

#> autoplot.ts ggfortify

#> fitted.ar ggfortify

#> fortify.ts ggfortify

#> residuals.ar ggfortify

require(ggplot2)

require(dplyr)

data(aud)

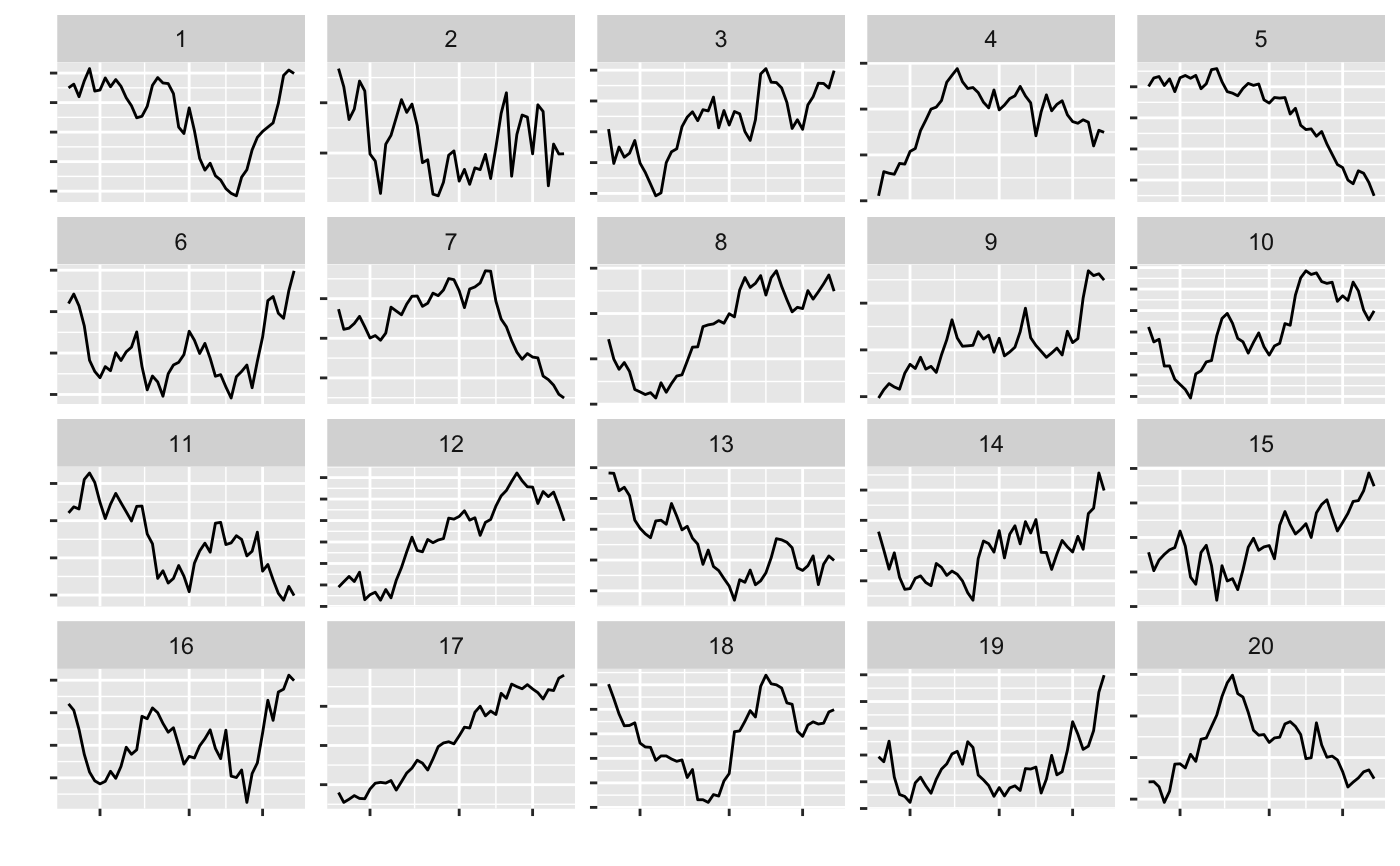

l <- lineup(null_ts("rate", auto.arima), aud)

#> decrypt("gwqp 2J5J c0 t8Zc5c80 Ao")

ggplot(l, aes(x=date, y=rate)) + geom_line() +

facet_wrap(~.sample, scales="free_y") +

theme(axis.text = element_blank()) +

xlab("") + ylab("")

l_dif <- l %>%

group_by(.sample) %>%

mutate(d=c(NA,diff(rate))) %>%

ggplot(aes(x=d)) + geom_density() +

facet_wrap(~.sample)

l_dif <- l %>%

group_by(.sample) %>%

mutate(d=c(NA,diff(rate))) %>%

ggplot(aes(x=d)) + geom_density() +

facet_wrap(~.sample)